The Crypto Crackdown Is Just Getting Started

But this ignores the bigger picture. In the first few weeks of 2023, watchdogs have done a lot. On Jan. 3, a joint statement by US bank regulators warned the industry of crypto risks creeping into the banking system. Then came a $100 million settlement with Coinbase Global Inc. over weak internal controls, a lawsuit against the Winklevoss twins’ Gemini and broker Genesis for allegedly selling unregistered securities, and a $45 million settlement with lending platform Nexo (which has ceased US operations). Subpoenas are flying.

The wheels of justice turn slowly — the Gemini and Genesis complaint came too late for customers fighting to get back $900 million in trapped funds — but they’re accelerating now. Regulators like the SEC rightly feel vindicated by the past year’s events, which saw a widespread loss of faith in crypto fail to snowball into a wider economic crisis. The collapse of FTX demonstrated the industry’s failings but also the benefits of a tough regulatory line on exchanges, such as when the SEC intervened behind the scenes in 2021 to ward Coinbase off launching its own crypto-lending product. As one official put it last year, the “runway is getting shorter” for unruly platforms.

There may be plenty of debate over whether crypto tokens are more like securities, commodities, shadow banking or gambling, but the ongoing focus is to ensure crypto’s troubles don’t leak into the financial system. While legislative attempts to craft crypto rules designed to prevent another “Lehman Brothers moment” run into procedural delays and embarrassing revelations about FTX’s history of cozy ties with Capitol Hill, regulators with long memories are keeping an active eye on banks’ crypto exposure as the real risk gauge. Silvergate Capital Corp., already crushed by its exposure to FTX, seems to have gotten the message and written down the value of stablecoin assets it bought from Meta Platforms Inc.’s Diem — worth almost $200 million at the time — to basically nothing.

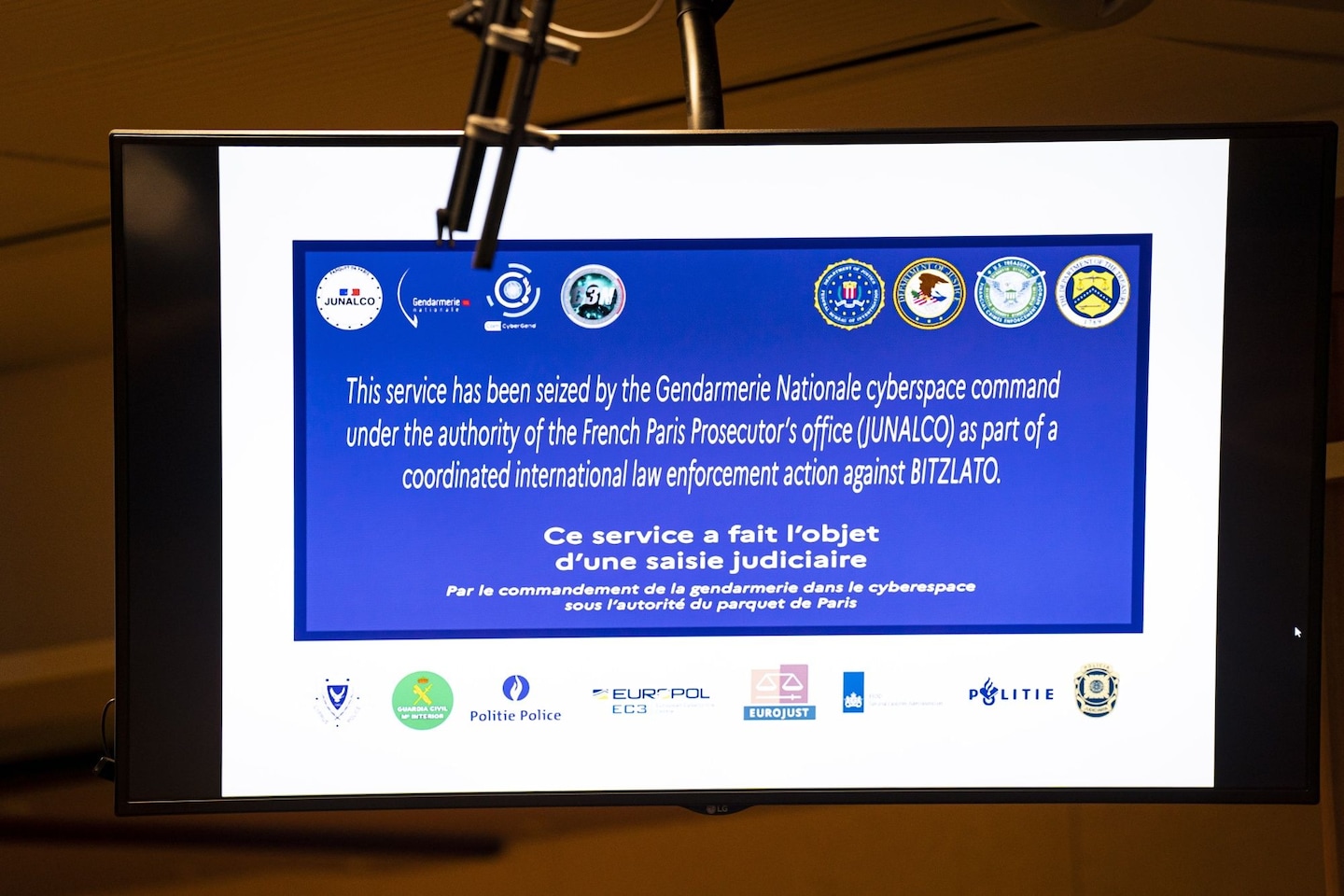

The Bitzlato action is part of this push, with the DOJ citing the exchange’s inadequate anti-money-laundering controls and “substantial” business with US customers — two examples of the kind of regulatory gaps in the system that missed FTX’s red flags. Carol Van Cleef, a lawyer with a long experience in digital assets, sees a blueprint for future actions, including the US Treasury’s determination that Bitzlato is a “primary money laundering concern,” rendering it effectively an international pariah. This goes beyond the SEC.

Regulation has critics. Some fear overreach; others think it counter-productive to try to build guardrails around digital assets rather than stepping back and letting it “burn.” It’s true that crypto is rife with activity that’s more gambling than investing. And it’s somewhat depressing to see that those at the heart of last year’s crypto collapse already have redemption in mind, from Three Arrows Capital to FTX.

But money laundering, fraud, market manipulation and tax evasion aren’t risks that just fix themselves. As the European Central Bank’s Fabio Panetta has pointed out, regulators see the costs to society of unregulated digital assets as high and requiring more action. The crackdown is clearly just getting started; those who are keen to dive back into crypto, even having just taken a bath, should take note.

More From Bloomberg Opinion:

• Crypto’s Hotel California Traps Winklevoss Twins: Lionel Laurent

• Matt Levine’s Money Stuff: Crypto Banks Owe Themselves Money

• Gold Is Getting Its Glitter Back: Merryn Somerset Webb

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering digital currencies, the European Union and France. Previously, he was a reporter for Reuters and Forbes.

More stories like this are available on bloomberg.com/opinion

Credit: Source link

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  Solana

Solana  Dogecoin

Dogecoin  USDC

USDC  Cardano

Cardano  Avalanche

Avalanche  Toncoin

Toncoin  Wrapped stETH

Wrapped stETH  Shiba Inu

Shiba Inu  Wrapped Bitcoin

Wrapped Bitcoin  Sui

Sui  Hedera

Hedera  Stellar

Stellar  Polkadot

Polkadot  WETH

WETH  Hyperliquid

Hyperliquid  Bitcoin Cash

Bitcoin Cash  LEO Token

LEO Token  Litecoin

Litecoin  Pepe

Pepe  Wrapped eETH

Wrapped eETH  NEAR Protocol

NEAR Protocol  Ethena USDe

Ethena USDe  USDS

USDS  Aave

Aave  Aptos

Aptos  POL (ex-MATIC)

POL (ex-MATIC)  Render

Render  WhiteBIT Coin

WhiteBIT Coin  Virtuals Protocol

Virtuals Protocol  Bittensor

Bittensor  MANTRA

MANTRA  Artificial Superintelligence Alliance

Artificial Superintelligence Alliance  Arbitrum

Arbitrum

Comments are closed.